Sustainability Reporting Accelerator

Social expectations of businesses and industries are increasing—in relation to Environment, Society and Governance (ESG) following the United Nations' adoption of the 2030 Agenda for Sustainable Development Goals (SDGs), and in relation to climate change following the Paris Agreement's adoption at the 21st Conference of the Parties (COP21). Many organisations are aligning their business to address the United Nations Sustainable Development Goals (SDGs) in order to create a cleaner, healthier, and more sustainable society.

We recently completed a project with a leading financial services provider in the UK, offering financial solutions to clients, brokers, and businesses of all sizes and specialisations. Retail point of sale finance, motor finance and personal loans, asset finance and invoice finance, and vehicle funding and fleet management are among the financial services provided by this client.

In order to help make achieving their sustainability targets a reality, the client required a number of reports to be generated to support the sustainability initiatives. Currently, the reports are generated manually by client's Corporate Social Responsibility (CSR) team. These reports are created by aggregating data from various sources across all business units.

The client were looking for a solution to automate the report generation with the use of their existing data lakehouse infrastructure. During previous engagements, Advancing Analytics designed, built, and implemented the current data lakehouse platform utilising the Hydr8™ framework. This Sustainability phase used data that was already onboarded to the data lakehouse platform to create multiple reports necessary for sustainability reporting.

Since 1 October 2013 the Companies Act 2006 (Strategic Report and Directors’ Report) Regulations 2013 have required all UK quoted companies to report on greenhouse gas emissions as part of their annual Directors' Report.

From 1 April 2019, quoted companies must report on their global energy use and large businesses must publish their UK yearly energy use and greenhouse gas emissions. This is required by the Companies (Directors’ Report) and Limited Liability Partnerships (Energy and Carbon Report) Regulations 2018.

The Companies (Directors’ Report) and Limited Liability Partnerships (Energy and Carbon Report) Regulations 2018 implement the government’s policy on Streamlined Energy and Carbon Reporting. These make amendments to the Large and Medium-sized Companies and Groups (Accounts and Reports) Regulations 2008 and the Limited Liability Partnerships (Accounts and Audit) (Application of Companies Act 2006) Regulations 2008 (‘the Regulations’).

To comply with regulations, our client is required to produce on a number of sustainability reports listed below:

Net Zero Full Financial Year Report

Green Bond Impact Report

Streamlined Energy and Carbon Reporting (SECR)

Annual Report and Consolidated Financial Statements

ESG Environmental Annual Report

Sustainable Business Reporting

Energy Saving Opportunity Scheme (ESOS)

TCFD Climate Risk

Carbon Reduction Plan (PPN06/21)

Prior to this engagement, the client was spending months manually collating this data across the estate and bringing it together in a series of Excel reports to satisfy regulatory reporting.

The reporting largely revolves around scopes of emissions, as visualised in the following diagrams:

Infographic explaining the Scopes from Plan A: https://plana.earth/academy/what-are-scope-1-2-3-emissions/

Scope 1 being the direct emissions from company owned or controlled resources, as a result of the business' activities. This could be the emissions related to the heating of company buildings or the use of company vehicles used to conduct business activities.

Scope 2 are the indirect emissions for upstream activities, such as the purchasing of generated electricity for the use by the business to conduct activities, and the emissions associated with that generation.

Scope 3 is divided between Scope 3a - indirect upstream emissions - and scope 3b - indirect downstream emissions.

Scope 3a are all indirect emissions relating to the upstream activities, which aid the business in its activities. These could be Purchased goods and services, business travel, employee commuting, any leased assets and many others.

Scope 3b are all indirect emissions relating to downstream activities, which is generated from the distribution, selling and aftercare of the value chain. These include investments made by the business, any assets that the business leases to end consumers (other businesses or individuals), and many others.

As part of this project, we created a common data model that would support these reporting requirements. There are two parts to this data model:

General Emissions

Downstream Emissions

General Emissions

This model seeks to track general emissions generated by the client. This is a combination of Scopes 1, 2 and 3.

Scope 1 & 2 emissions are largely focused on the emissions generated by the client themselves. This includes such examples as:

Combustion generated by company cars – business travel

Combustion generated by company cars - employee commuting

Stationary combustion provided by natural gas - Heating offices

Purchased electricity

Scope 3a emissions are more complicated, they focus on the direct impact of the client running as a business, such as:

Purchase goods and services – Services consumed in the running of the client's business.

Capital goods – Fixture, fittings and other client owned assets.

Fuel and energy related – Waste from used energy (Well to tank, distribution losses)

Waste generated operations – Solid waste & Water waste

Business travel

Employee commuting

Where an overlap in scope is observed, the data model will be designed in such a way to ensure that there is no double counting or double reporting of these numbers. The same logic extends when looking at scope 3b, where vehicles used for business travel are part of the client’s fleet provided by a business unit.

Conceptual Data Model for General Emission subject area

Downstream Emissions

This data model tracks downstream emissions generated by the client where emissions are generated as part of Scope 3b – Indirect emissions. This included examples such as:

Type of Loans made to customers

Leased assets to customers

Conceptual Data Model for Downstream Emission subject area

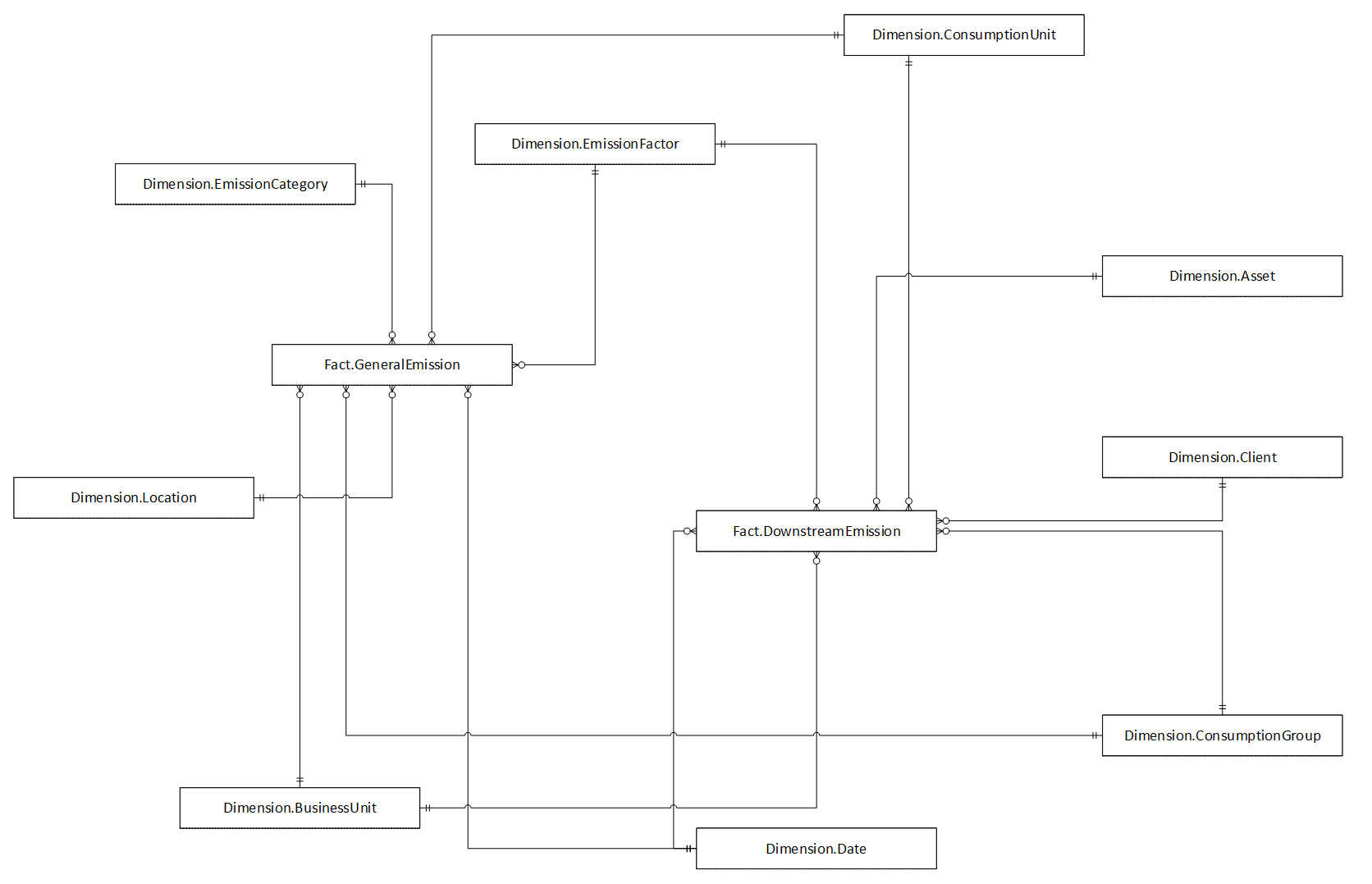

Conformed Data Model

While we have two data models, we have conformed the two data models into a single physical data model, reflecting their shared dimensions and contexts.

Conformed Data Model bringing together the two subject areas

By creating a conformed data model, it allowed our client to create multiple reports off the same data model using Power BI, with data served to Power BI using Databricks SQL in conjunction with Delta.

Call-To-Action

As Sustainability Reporting is a legal requirement for Quoted Companies to carry out in the UK, by investing in the automation of the reporting requirements allowed this client to save months on manual effort each year in collating this data and information. It also gave the team responsible for Sustainability more time back to provide greater value in making strategic decisions to reduce the overall emissions and further the journey to Net Zero and Sustainability.

If you are finding your company spending lots of time manual collating data for regulatory reporting or are wanting to improve your sustainability reporting, please contact Advancing Analytics today where we can utilise our Hydr8™ framework and Sustainability Reporting solution accelerator to help you quickly meet your needs.